Rhode Island's New Non-Owner Occupied Property Tax ("Taylor Swift Tax"): What Every Homeowner Needs to Know (2026)

If you're searching for information about Rhode Island's new Non-Owner Occupied Property Tax—better known as the "Taylor Swift Tax"—you're probably asking one simple question:

"Does this apply to me?"

You're certainly not alone.

Over the past several months, I've had conversations with homeowners throughout Narragansett, Jamestown, South Kingstown, North Kingstown, and other coastal communities who are asking many of the same questions.

Will I owe this tax?

How much could it cost me?

Could this affect the value of my home?

Should I be thinking differently if I plan to keep my property for another ten years?

If I'm considering selling, does this change anything?

Those are the questions this guide is designed to answer.

Despite the nickname, this isn't simply a tax on celebrities or owners of sprawling oceanfront estates. It has the potential to affect thousands of Rhode Island homeowners—including many families who purchased modest beach cottages decades ago, inherited seasonal homes, or own vacation properties they hope to retire to someday.

In South County especially, that matters.

A cottage purchased for a few hundred thousand dollars thirty years ago may now carry a municipal assessment exceeding $1 million—not because the house changed dramatically, but because the house and land became far more valuable. That's why so many longtime owners are paying attention.

As a Realtor specializing in South County Rhode Island, my goal isn't to debate the law or offer legal advice. It's to help homeowners understand how the law works, clear up some of the confusion surrounding it, and explain what I believe owners should be thinking about as they evaluate one of their biggest financial assets.

Whether you're planning to keep your property, purchase another home, or eventually sell, understanding this new tax has become part of owning real estate in Rhode Island.

| Important: This article is intended for general informational purposes only and should not be considered legal or tax advice. Every homeowner's situation is different. If you have questions about your specific circumstances, consult your attorney or tax professional.

Does This Tax Apply to You? Start Here.

You don't need to read a 3,000-word article to know whether this tax might apply to you.

Start with these four questions.

1. Is your property's municipal assessed value over $1 million?

If the answer is no, you can probably stop reading.

If the answer is yes, keep going.

This is also one of the biggest points of confusion.

| Remember: The law uses your municipal assessed value—not your Zestimate, a recent appraisal, or what you paid for the property. This is the assessed value assigned by your city or town that appears on your annual property tax bill and is used to calculate your local real estate taxes.

In other words, don't assume your home's current market value tells you whether this tax applies.

Your municipal assessment is the number that matters.

2. Is this your primary residence?

For most homeowners, this is the next question.

Generally speaking, if the property is your primary residence and you occupy it for at least 183 days during the privilege year, the new tax doesn't apply.

For many South County homeowners, the answer is straightforward.

For others, it's not.

Perhaps you split your time between Rhode Island and Florida.

Maybe you spend every summer at your beach house but live elsewhere the rest of the year.

Or maybe you're planning to retire here in a few years but aren't living here full-time yet.

Those situations deserve a closer look before making assumptions.

3. Does your property qualify for one of the rental exemptions?

The law includes exemptions for certain long-term and short-term rental properties, but many homeowners misunderstand how they work.

One of the biggest misconceptions I've heard is:

"I listed it on Airbnb, so I'm probably exempt."

Not necessarily.

Simply making your property available for rent isn't enough.

The property actually has to meet the state's rental requirements to qualify.

If you're counting on one of these exemptions, it's worth taking the time to understand exactly what the law requires before assuming it applies.

We'll cover those exemptions in more detail shortly.

4. Are you relying on facts—or Facebook?

That might sound funny, but it's become one of the biggest challenges surrounding this new law.

I've heard homeowners confidently repeat things like:

"My neighbor said nobody has to pay it."

"Someone told me it only applies to mansions."

"I heard putting the house into a trust avoids it."

"If I rent it for the summer, I'm automatically exempt."

Unfortunately, many of those statements are incomplete—or simply wrong.

That's one reason I wanted to write this guide.

There's a lot of noise surrounding Rhode Island's new Non-Owner Occupied Property Tax.

My goal is to separate the headlines from the facts.

Why This Law Has So Many South County Homeowners Talking

Most headlines focus on Taylor Swift.

Personally, I think that's missing the real story.

The homeowners I talk with aren't celebrities.

They're teachers.

Retirees.

Business owners.

Families who've spent every summer in the same cottage for thirty years.

People who bought a vacation home long before anyone imagined what coastal Rhode Island real estate would be worth today.

In communities like Narragansett, Jamestown, Charlestown, and South Kingstown, it's remarkably common for a modest seasonal home to sit on land that's appreciated dramatically over the past several decades.

That's created a situation where many homeowners suddenly own property assessed above $1 million—even though they don't necessarily consider themselves owners of "luxury real estate."

That's why this law has generated so much conversation.

It's not simply about another tax.

It's about the changing economics of owning a second home in Rhode Island.

So... What Exactly Is Rhode Island's New Non-Owner Occupied Property Tax?

Rhode Island's Non-Owner Occupied Property Tax took effect on July 1, 2026 as part of the state's annual budget.

Unlike your local property tax—which is set and collected by your city or town—this is a statewide tax that applies to certain residential properties with a municipal assessed value exceeding $1 million that are not occupied as the owner's primary residence.

That's an important distinction.

Many homeowners already pay different local tax rates depending on where they live. This new law doesn't replace those taxes—it sits alongside them.

The revenue generated by the statewide tax is intended to support affordable housing initiatives across Rhode Island.

Whether you agree with the policy or not, the law is now in effect, and many homeowners have already begun receiving notices from the Rhode Island Division of Taxation.

For some owners, the notice confirmed what they expected.

For others, it came as a surprise.

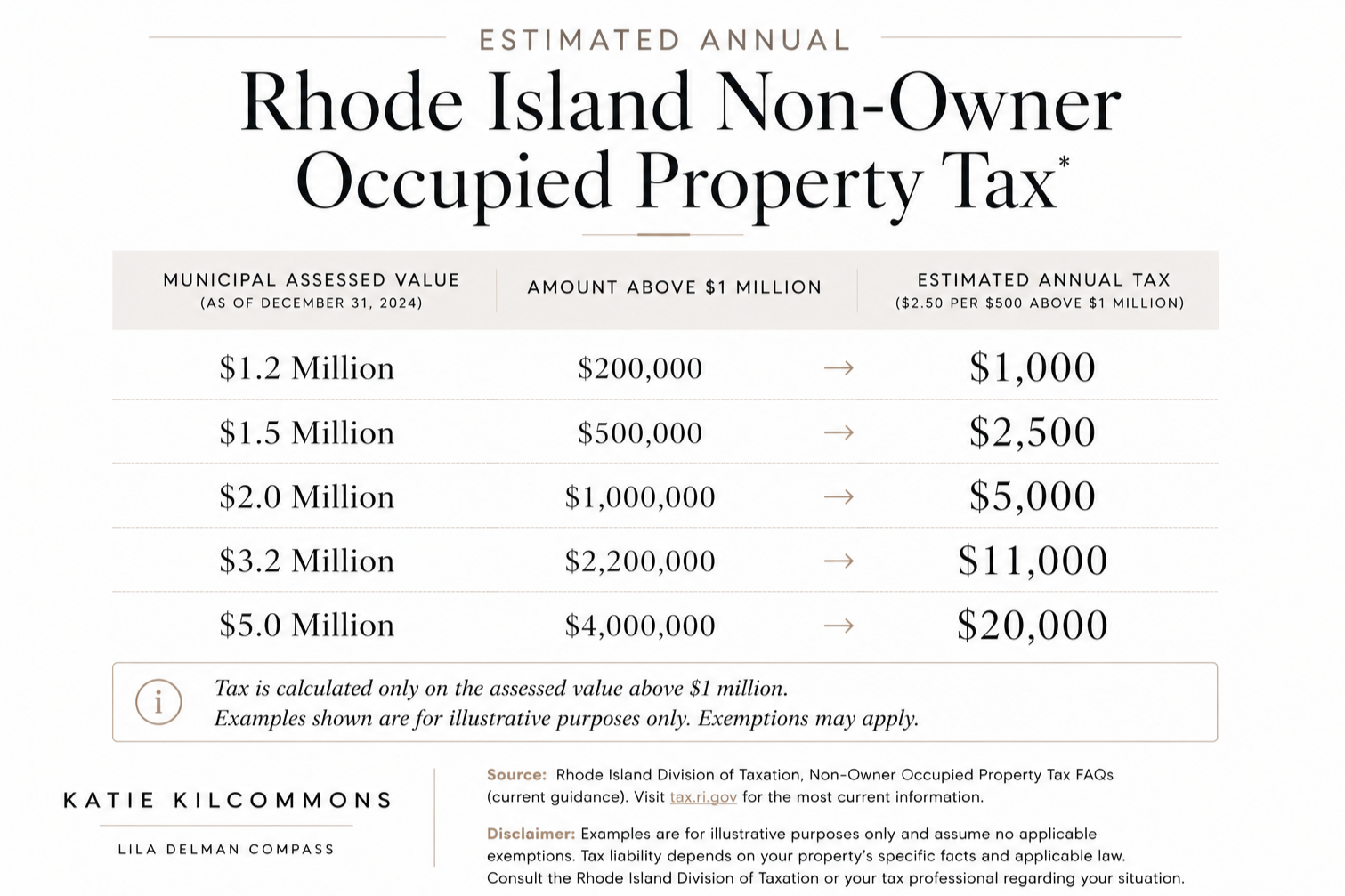

How Much Could You Owe?

The tax itself is fairly straightforward.

Rhode Island charges $2.50 for every $500 of assessed value above $1 million.

Here's what that looks like using a few examples.

For some homeowners, that's an expense they can comfortably absorb.

For others, particularly those who only use their property a few weeks each year, it's another line item added to an already growing list of ownership costs.

And that's where I think the conversation becomes much more interesting.

Because in my experience, homeowners rarely evaluate one expense in isolation.

Common Misconceptions About Rhode Island's New Non-Owner Occupied Property Tax

Whenever a new law is introduced, misinformation spreads almost as quickly as the headlines.

Since Rhode Island's Non-Owner Occupied Property Tax was announced, I've heard homeowners confidently repeat information they read online, heard from a neighbor, or saw discussed on social media—only to discover later that it wasn't entirely accurate.

Here are a few of the most common misconceptions.

"My home is worth more than $1 million, so I automatically owe the tax."

Not necessarily.

One of the biggest misunderstandings is confusing market value with municipal assessed value.

The statewide tax is based on your municipality's assessed value—not what Zillow estimates your home is worth, what a recent appraisal says, or what you could sell it for today.

Even if your municipal assessment exceeds $1 million, factors such as whether the property is your primary residence or qualifies for one of the statutory exemptions still matter.

"I only use my house during the summer."

Many South County homeowners spend summers in Rhode Island while living elsewhere the rest of the year.

That alone doesn't determine whether the tax applies.

The important questions become:

Is this your primary residence?

Do you occupy it at least 183 days during the privilege year?

Does the property qualify for one of the available exemptions?

Each homeowner's situation is different, which is why assumptions can quickly become expensive.

"If I rent it, I'm automatically exempt."

This is another misconception I hear frequently.

Simply advertising your home for rent—or even renting it for part of the summer—doesn't automatically exempt the property.

Rhode Island established specific requirements for qualifying long-term and short-term rental exemptions. If you're relying on one of those exemptions, it's important to understand exactly what the law requires before assuming your property qualifies.

"I'll just create a lease for $1."

This question has come up surprisingly often.

I've heard homeowners ask whether they could simply create a written lease for a nominal amount—say, $1 per month—for 183 days and qualify for an exemption.

While I understand why people are asking, I would strongly encourage homeowners not to assume that approach would satisfy the law.

Rhode Island's Division of Taxation has the authority to review exemption claims and request supporting documentation. If you're considering any strategy specifically intended to qualify for an exemption, it's worth discussing with your attorney or tax professional before making assumptions.

"My home is owned by a trust."

Trust ownership doesn't automatically determine whether the tax applies.

Depending on the circumstances, a property held in trust may still qualify as a primary residence or otherwise be treated differently under the law.

If your home is owned through a trust, this is one area where professional legal advice is especially important.

What Makes South County Different?

This is where I think the conversation becomes unique.

Unlike many parts of Rhode Island, South County has an unusually large number of second homes, vacation properties, seasonal cottages, and waterfront residences.

Families often purchase these homes with the intention of keeping them for generations.

Others inherit a family cottage that becomes part of every summer.

Many buyers I've worked with aren't purchasing an investment property at all—they're purchasing a future retirement home or a place where children and grandchildren can gather.

That's why I don't believe it's helpful to think about this law simply as another tax.

For many homeowners, it's another ownership cost that now joins a growing list of annual expenses.

Property taxes.

Insurance.

Flood insurance.

Maintenance.

Utilities.

Repairs.

HOA fees.

And now, for some owners, Rhode Island's new Non-Owner Occupied Property Tax.

Every homeowner's financial picture is different.

For one family, this tax may have little impact.

For another, it may be the expense that finally causes them to reconsider whether keeping a second home still makes sense.

Could This Affect Home Values?

This is probably the question I've been asked more than any other.

The honest answer is:

No one knows for certain.

Whenever ownership costs increase, buyers naturally take notice.

That doesn't necessarily mean home values decline.

In fact, South County remains one of the most desirable coastal markets in New England, and demand for waterfront and vacation properties continues to be driven by factors that extend well beyond one annual expense.

What I do think will happen is that buyers will continue asking more questions.

They're already evaluating:

Property taxes

Homeowners insurance

Flood insurance

Utility costs

Deferred maintenance

Future capital improvements

This new tax simply becomes another part of that conversation for properties where it applies.

As a result, sellers should expect well-informed buyers who are looking carefully at the total cost of ownership—not just the purchase price.

What Sellers Should Know

If you're thinking about selling a second home, vacation property, or waterfront residence, I don't see this new tax as a reason to panic.

What it does reinforce is something I've already been seeing throughout the South County market: today's buyers are paying closer attention to the total cost of ownership than they were just a few years ago.

They're looking beyond the purchase price and evaluating annual property taxes, homeowners insurance, flood insurance (where applicable), maintenance costs, utilities, and now, for some properties, Rhode Island's new Non-Owner Occupied Property Tax.

That doesn't necessarily mean buyers will pay less for your home. Coastal Rhode Island remains one of the most desirable places to own real estate in New England. It simply means buyers are asking more questions and making more informed decisions before submitting an offer.

If you're considering selling, having the right pricing strategy, thoughtful marketing, and a clear understanding of what today's buyers are comparing has never been more important.

Final Thoughts

Rhode Island's new Non-Owner Occupied Property Tax has generated plenty of headlines, but the real story is much simpler.

Homeowners aren't looking for political debate—they're looking for clarity.

They want to know whether the law applies to them, how it's calculated, whether they qualify for an exemption, and how it fits into the bigger picture of owning a second home in Rhode Island.

While this new tax may become another annual ownership expense for some property owners, it doesn't change what has always made South County such a special place to own a home.

People continue buying property here because of the lifestyle.

The beaches.

The boating.

The coastal villages.

The traditions of gathering with family and friends year after year.

Those reasons haven't changed.

If you own a second home or vacation property, my advice is simple: understand how the law applies to your specific situation, evaluate it alongside your other ownership costs, and make decisions based on your family's long-term goals—not just the latest headline.

Before You Decide to Keep, Rent, or Sell Your Second Home...

I'd encourage every homeowner to ask themselves:

Do I know my property's current municipal assessed value?

Have I confirmed whether I qualify for an exemption?

How much does it really cost me to own this property each year?

If I sold today, would keeping the property still make the most financial sense for my family?

Am I making this decision based on headlines—or based on my own long-term goals?

Related Resources for Rhode Island Homeowners

If you found this guide helpful, you may also enjoy these articles:

Or, if you're just beginning your research, you can explore my full collection of Rhode Island home selling resources here: Selling a Home in Rhode Island Resource Center

About the Author

Katie Kilcommons is a Sales Associate with Lila Delman Compass, specializing in waterfront, luxury, and coastal real estate throughout South County, Rhode Island.

She works with buyers and sellers in Narragansett, Jamestown, South Kingstown, Charlestown, North Kingstown, and the surrounding coastal communities, helping homeowners make informed decisions about pricing, marketing, and the complexities of coastal property ownership.

Katie was recognized as one of the Top 10 real estate agents in Narragansett, and has also been recognized as a RealTrends Verified Agent and a Five Star Professional.

This article is intended for general informational purposes only and should not be considered legal or tax advice. Homeowners should consult the Rhode Island Division of Taxation, an attorney, or a qualified tax professional regarding their specific circumstances.